Economic and Property Overview: Q1 2019

UK ECONOMIC OVERVIEW

Economic growth was relatively buoyant at the start of the year, output grew by 0.5%mom in January and by 0.2%mom in February, offsetting the 0.4% contraction in output in the final month of 2018. However, much of this growth spurt was driven by temporary factors such as a pick-up in manufacturing activity from firms stockpiling goods to shield against a disruptive Brexit.

Brexit preparations had a positive impact on business sentiment too, the manufacturing PMI rose 300bps to 55.1 in March, but the large upswing contrasts to the direction of travel on other PMI indices; the construction PMI increased fractionally from 49.5 to 49.7 over the month, while the services PMI fell into contractionary territory (below 50) for the first time in two and a half years. The overall composite score of 50.6 (down from 51.4 in February) suggests that GDP growth will stagnate over the rest of the year.

The labour market shows no signs of slowing; an additional 179,000 people entered the workforce over the three months to February, raising the total number of people in work to a high of 32.7 million. The number of people in unemployment also fell by 27,000, keeping the unemployment rate sub 4% for the second month running .This expansionary phase is likely to persist in the near term, job vacancies continue to rise month on month with 852,000 positions recorded in March, the 15th consecutive month of 800,000+ vacancies. Moreover, improving labour market conditions are being converted into higher earnings, average weekly earnings excluding bonuses rose by 3.4%yoy in January and by 1.5%yoy in real terms.

The annual rate of CPI inflation remained unchanged over the month to 1.9%, within a whisker of the Bank of England’s (BOE’s) 2% inflation target. The main upward contributions came from transport, where prices fell in the month to March, but by less than between the same two months a year ago. Downward contributions came from recreation and culture where prices rose but by less than the same point last year. The government’s proposal to raise the energy price cap in April, should cause inflation to tick upwards in the short term. Yet, despite the risk of rising inflation pressures and continued wage gains, the BOE voted to keep the base rate at 0.75% in March, citing increased Brexit anxiety and slower global growth prospects as key concerns to the economy’s short term growth outlook.

Retail sales volumes rose by 0.4% over the month to February and 4% on a year earlier, according to the Office for National Statistics. Non-store retailing (particularly fuel sales and online shopping) provided the largest contribution to growth, while the unusually warm weather boosted spend at garden centres and on sporting equipment. A separate measure compiled by the British Retail Consortium which tracks total retail sales for the major high street retailers and supermarkets across the UK reported a 0.6% rise in retail sales over the first three months of the year, a third of the growth rate recorded for the same period a year earlier (1.8%).

Brexit. Will it happen? Won’t it happen? It has been nearly three years since the nation voted to leave the European Union and businesses and consumers are still unsure of how the saga will conclude. After three meaningful votes on the Prime Minister’s withdrawal agreement were rejected, a series of indicative votes by the House of Commons on an alternative form of Brexit arrangement proved unfruitful, including a vote on a “no-deal” Brexit which was vehemently voted down, the European Council finally agreed to grant the UK a second extension to Article 50, shifting the Brexit deadline to the 31st October. A cross-party approach is now being sought by the Government as a way out of the Brexit impasse, with a closer post-Brexit relationship with the EU being the preferred route of choice. As things currently stand, the risk of the UK leaving without a deal or a general election cannot be discounted.

UK PROPERTY MARKET PROSPECTS

The commercial property market started the new year on a softer note. The All Property total return on the MSCI Monthly Index was 0.5% for the three months to March 2019, down from 1.1% for the three months to December. The All Property income return remained unchanged at 1.3% for the quarter, which meant that all of the downward pressure on performance came from capital growth, which contracted by 0.8% over the period. The retail sector delivered the largest capital declines over the quarter, with capital falls ranging from –0.5% for London retail to a low of -5.2% for department stores. Unlike previous months, capital falls were not solely contained to the retail sector, with City offices, South East offices and the leisure sector also reporting minor declines in asset values of –0.5%, -0.1% and -0.7% respectively.

Occupational activity was muted across all property sectors in Q1. According to CBRE, Central London office take-up was lower in January and February of this year, than the same periods a year earlier, while take up of 100,000sqft+ industrial units totalled 4.9m sq ft in Q1 2019, approximately half the level recorded in Q1 2018 according to Colliers Industrial and Logistics Barometer report. Meanwhile, the retail sector continues to deliver its share of bad news, Office Outlet, LK Bennett and Debenhams were just a few of the retailers that entered administration in 2019 and Thomas Cook, Arcadia, Boots, Kingfisher and Majestic Wine some of the latest retailers to announce store closures. Weaker occupier demand caused All Property rental values to flat line over the quarter. On a sectoral basis, rental values across the retail and other segments declined by 1.0% and 0.4%. All other main use sectors (offices and industrials) reported positive rental value growth of 0.5% and 0.7% respectively.

Investment market activity weakened in the first two months of the year, as investors awaited further clarity on the Brexit outcome before committing to investments. The total value of commercial property deals was £1.5bn in February, half of the value recorded in January of £3bn. Reduced rental value growth expectations and weakening investor sentiment towards property caused property yields move out for the third month in a row, the All Property initial and equivalent yield now sits at 5.02% and 5.86% respectively, 9bps and 4bps higher than at the end of 2018.

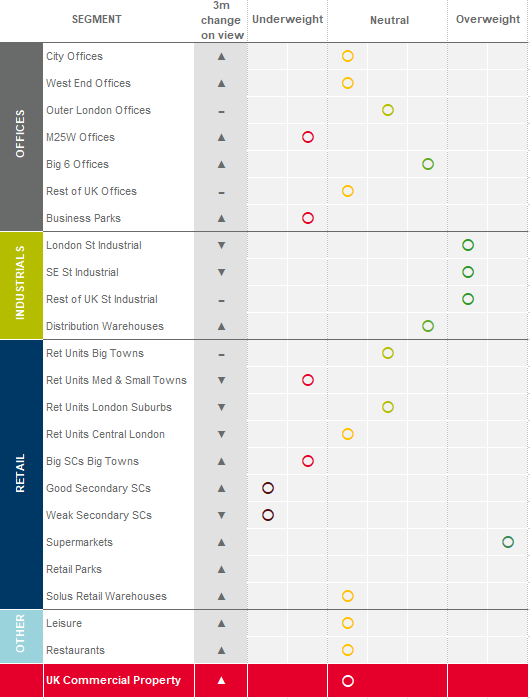

Looking forward, lingering Brexit concerns, continued weakness in retail markets and a further softening in property yields are expected to weigh on performance prospects over the remainder of the year. Against this backdrop, industrials, regional offices and the alternative segments look better positioned and should deliver the best absolute total returns in 2019.

View our latest outlook on the each sector here.

{kind=link}